We might think the main economic news in Australia right now is interest rates and the new historic low cash rate of 1.00%. It is big news of course, but the really significant issue is why it has occurred. The Australian economy is in a consumption decline that sees the Reserve Bank of Australia (RBA) seeking to free up liquidity (by lowering interest rates) to encourage spending. Source: Timberbiz

Historically that worked, but increasingly, the bluntest tool of monetary policy has been found lacking for a variety of reasons. Not least of these is that consumers have, generally speaking, been using lower interest rates as a means of reducing indebtedness or at least standing still.

So, in and of themselves, lower interest rates are not as likely to prime the economic pump, as was previously the case. Expectations of further interest rate cuts may be more stimulatory, but we would not count on it.

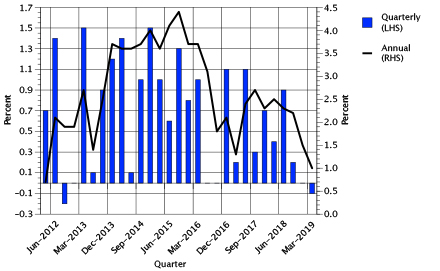

Essentially, Australia’s consumers have had their ‘queues in the rack’ over the last year or more. We can see in the chart that over the year-ended March, retail sales grew a very sickly 1.0% in cash terms. That is below the also anaemic inflation rate of 1.3% for the same period, meaning that in real terms, retail sales went backwards.

Worse, Australia’s population grew by 1.6% over the year-ended March 2019, so on a per capita basis, retail sales continued to decline, recording something close to -0.9% per annum.

That data feeds into the emerging idea that Australia is in the grips of a ‘per capita recession’. That is, the only growth recorded is because of net population increases.

Little wonder then that the RBA Board has pulled the trigger on lowering interest rates, in what many expect will be two and some suggest as many as four rate cuts over the next year.

However, by early June, discussion had turned to the prospect of Australia engaging in a program of what is known as Quantitative Easing or QE. Much deployed in the US, Europe and Japan post the GFC, a program of QE involves central banks such as the RBA, releasing large amount of money that is currently held on the RBA balance sheet, into the economy.

The RBA would do this by buying up Government bonds or high quality corporate bonds, providing funds that would flow into the economy to support a wide range of activities – everything from infrastructure spending to new industrial developments.

In addition, a QE program would see interest rates full further, because the purchase of significant value of bonds, normally sees their price rise and the yield from them (interest rates for them) fall.

It is not clear that QE will proceed in Australia, but if direct interest rate cuts do not provide consumer-side stimulation, the RBA will be likely to turn its attention to the wholesale debt market. QE would be its most likely tool.

Every month, IndustryEdge publishes Wood Market Edge, Australia’s only forestry and wood products market and trade analysis, and supplies its customers with hundreds of unique data products, advisory and consulting services. Find out more at www.industryedge.com.au