Demand for the main paper grades used to supply catalogues and magazines continues to slump, with imports especially hard hit. Light Weight Coated (LWC) grades of paper made from mechanical pulp have seen imports crash more than 73% over the last two years, falling to just 26.4 kt year ended May 2021. Source: IndustryEdge

To place the declines into context, year-ended May 2014, imports peaked at 192.3 kt, more than seven times higher than was recorded just seven years later. It is no coincidence that in 2014, Norske Skog commissioned its LWC production capacity at the Boyer mill.

Production data can only be obtained annually, but we estimate production was no more than 100,000 tonnes over the last year, with the likelihood total consumption was around 125,000 tonnes. That would equate to about 25% less demand than a year earlier.

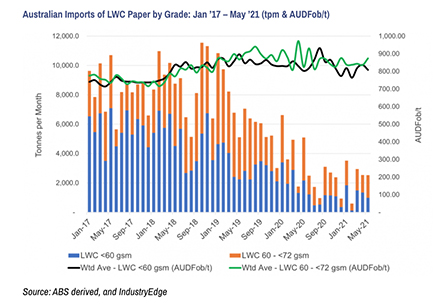

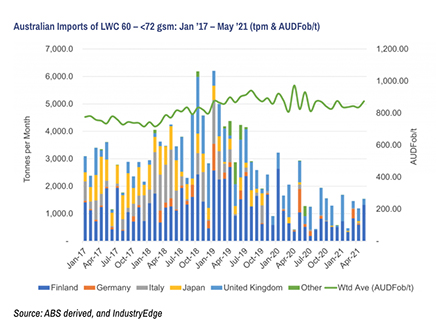

The chart below shows imports of the two LWC sub-grades, the <60 gsm and the 60-<72 gsm products.

Any coated paper made from primarily mechanical pulp is designated a Medium Weight Coated (MWC) paper.

The incredibly large drop in imports of both grades can be seen plainly, especially as it relates to the last year.

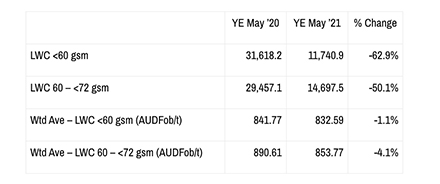

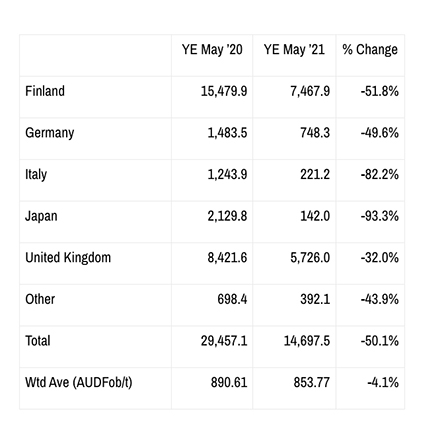

As the table shows, imports of the lighter-weight <60 gsm grade crashed by 63%, while the higher-grammage 60 – <72 gsm grade saw imports literally halved over the year.

Notably, weighted average import prices did not move markedly over the year, despite the slump in shipments.

IndustryEdge understands that given the price of pulp through much of the year, buyers were fortunate not to face price increases, regardless of the reduced volumes.

The simple reality is that demand for LWC paper grades has crashed because catalogues, including those produced as in-house magazines by Coles and Woolworths, are no longer being consumed.

Advertisers are migrating from catalogues at the fastest rate in history. They will not, in all likelihood, return. What the data points to is imports slipping further, as demand also continues to recede.

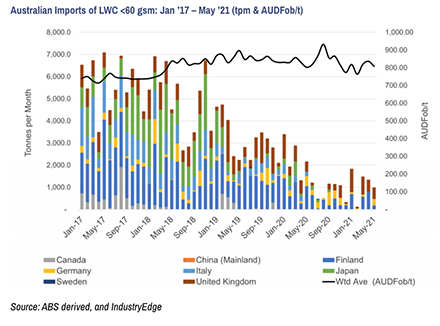

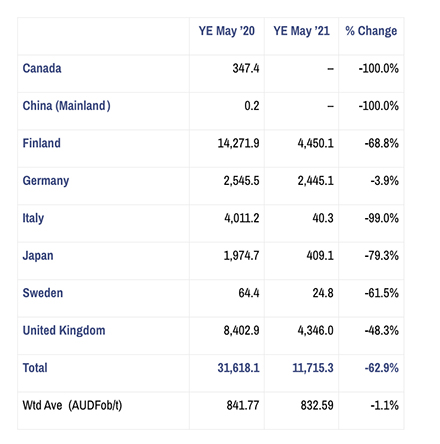

Finland is the significant supplier nation, delivering the largest volume of LWCs of both grammages over the last year. There are other suppliers across the grammages, but none comes close to the Finnish contribution.

The following charts and tables provide the details of the two grades and the supplier nations.

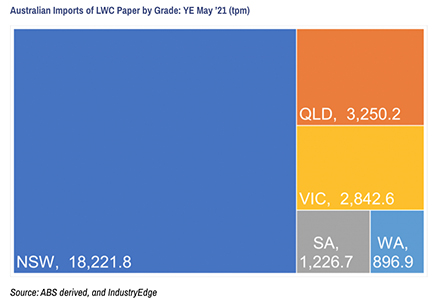

Considered on a state-by-state basis, LWC imports tell a story of a different type. The chart below emphasises how significant the consolidation of printing activity has become in Australia. More easily serviced from the local producer in Tasmania, imports to Victoria have fallen away, with the vast majority of LWCs delivered into New South Wales over the last year.